Table of Content

Keep in mind, though, that you’ll pay interest on them if you choose that option. The total of your monthly debt payments divided by your gross monthly income, which is shown as a percentage. Your DTI is one way lenders measure your ability to manage monthly payments and repay the money you plan to borrow. Our affordability calculator will suggest a DTI of 36% by default. You can get an estimate of your debt-to-income ratio using our DTI Calculator.

On conventional loans, for example, lenders usually like to see debt-to-income ratios under 43 percent, although in some cases, 50 percent is the cutoff. If you want to shrink your debt-to-income ratio before applying for a mortgage — which is a good idea — pay off your credit cards and other recurring debts like student loans and car payments. Once you close on your home loan, your monthly mortgage payment may well be the biggest debt payment you make each month, so it’s important to make sure you can afford it. Along with the down payment, this is probably one of the two biggest factors that determine how much you can afford. This is calculated by dividing your mortgage payment into your gross monthly income and converting it to a percentage. Our calculator also includes advanced filters to help you get a more accurate estimate of your house affordability, including specific amounts of property taxes, homeowner's insurance and HOA dues .

How To Determine Your DTI Ratio

The total will vary depending on what your lender charges, whether you’ll pay real estate transfer taxes and if the seller agrees to cover a portion of the fees. As you’re budgeting for a home purchase, it’s wise to plan for between 2 percent and 5 percent of the home’s purchase price. So, if you’re buying a $400,000 home, your closing costs might range between $8,000 and $20,000. Some lenders might give you the option to roll those costs into the loan to avoid paying for them out-of-pocket.

Eligible active duty or retired service members, or their spouses, can qualify for down payment–free mortgages from the U.S. These loans have competitive mortgage rates, and they don't require PMI, even if you put less than 20 percent down. Plus, there is no limit on the amount you can borrow if you’re a first-time homebuyer with full entitlement.

When you’re ready for a change, we’re ready to help.

The main benefit of an adjustable-rate loan is starting off with a lower interest rate to improve affordability. Avoid PMI. A down payment of 20 percent or more gets you off the hook for private mortgage insurance . A 10% down payment would make your monthly payment $1,243 per month, plus at least another $67 a month for PMI, for a total of $1,310. For example, if you make $3,000 a month ($36,000 a year), you can afford a mortgage with a monthly payment no higher than $1,080 ($3,000 x 0.36). Your total household expense should not exceed $1,290 a month ($3,000 x 0.43). This is the total amount of money earned for the year before taxes and other deductions.

My suggestion is to plug the numbers into this Nerdwallet calculator and see what makes sense. Notice, the longer you stay in the home, the more likely it is that you will save money. If you make 250k a year just save for like 6 months and you will have a downpayment for a 550k house. Or get it with PMI on a loan where PMI drops when you have 20% equity then pike savings into equity for 6 months to get rid of PMI.

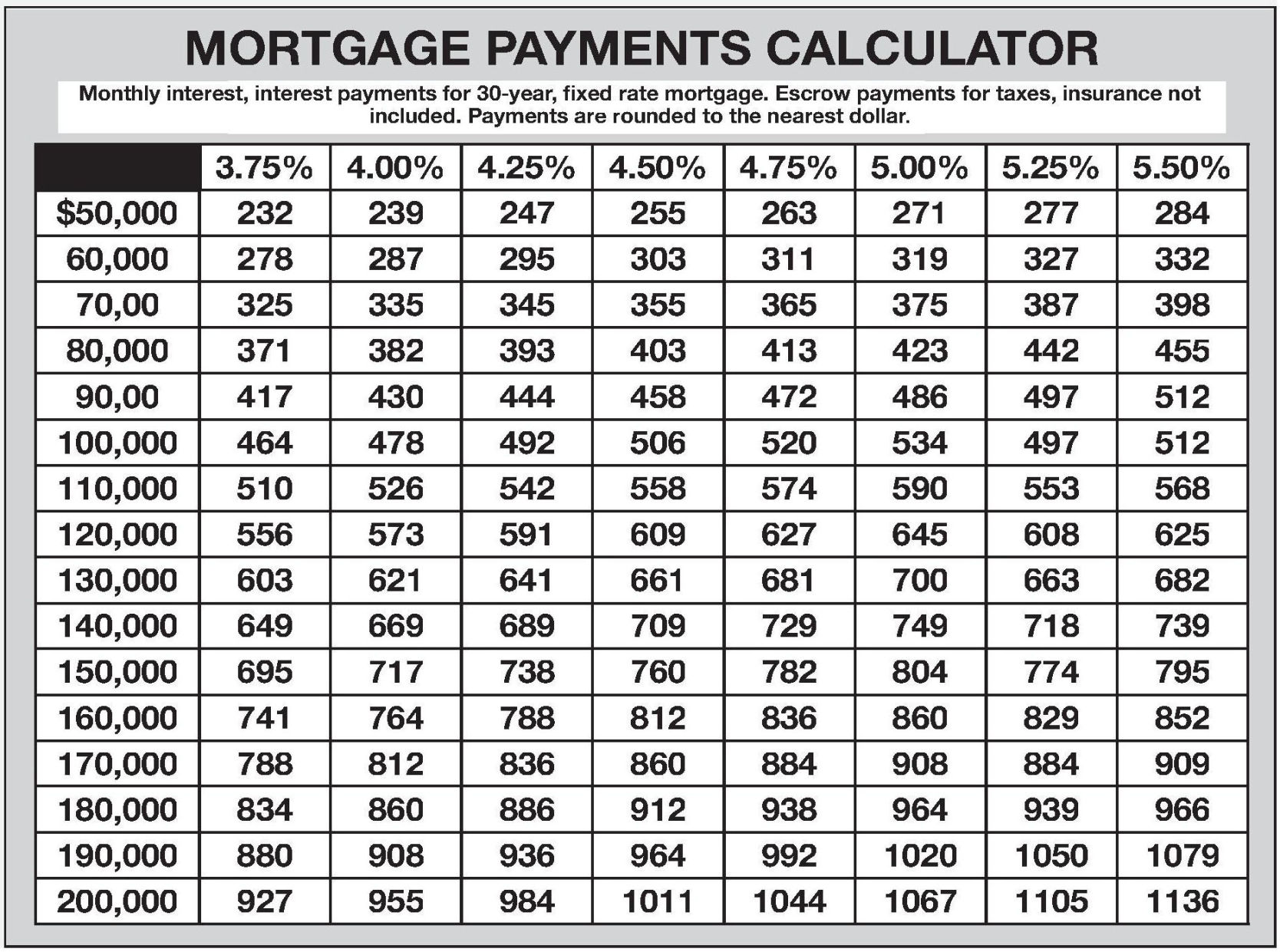

How Many Years Can I Knock Off My Mortgage Calculator

However, this loan typically requires private mortgage insurance which should be added into your monthly expenditures. PMI is usually .05-1% of the cost of the home loan but may vary depending on credit score. Many lenders commonly require private mortgage insurance if a borrower contributes less than a 20% down payment on a home purchase. PMI protects the lender against losses that may occur when a borrower defaults on a mortgage loan. Our calculator bases the PMI on the home price and down payment amount. You can choose to include or exclude PMI in the advanced options of the affordability calculator.

FHA loans are restricted to a maximum loan size depending on the location of the property. For most borrowers, the total monthly payment sent to your mortgage lender includes other costs, such as homeowner’s insurance and taxes. If you have anescrow account, you pay a set amount toward these additional expenses as part of your monthly mortgage payment, which also includes your principal and interest.

Mortgage term refers to the length of time you have to pay back the amount you’ve borrowed. The most common loan terms are 15 and 30 years, though there are other terms available. Unless you are concerned that your income will be interrupted I would not bat an eye paying 4200 mortgage when you takehome like 17k after taxes. Using a housing budget calculator to estimate what that all in number should be is a good idea, McBride says. List out your expenses and then add them together to get your total monthly spending.

Check your buying power by getting pre-qualified for a mortgage with us at Zillow Home Loans. Refinance calculatorInterested in refinancing your existing mortgage? Even though you may qualify for the amount listed above, it may not be suitable for you.

Lenders add all your debt to your new house payment and then divide it by your income, and most prefer a DTI ratio of about 43%. A home affordability calculator is a great starting point for determining the home price you might qualify for. For the Adjustable-Rate Mortgage product, interest is fixed for a set period of time, and adjusts periodically thereafter. At the end of the fixed-rate period, the interest and payments may increase. If you get rid of the $85 monthly credit card payment, for example, your DTI would drop to 39 percent.

Most loan programs require at least a 3% to 3.5% down payment. Department of Agriculture , offer no-down-payment programs to eligible borrowers. If you’re not sure, type in how much money you’ve saved or could save for a down payment.